Netflix sees first decline as competition heats up

Half of Australians deem on-demand services essential for entertainment

SYDNEY, AUSTRALIA – The Australian subscription entertainment market, which includes video, music and gaming services, saw a slowdown in annual growth in the past 12 months due to the rising cost of living pressures, according to a new study from leading Australian emerging technology analyst firm Telsyte.

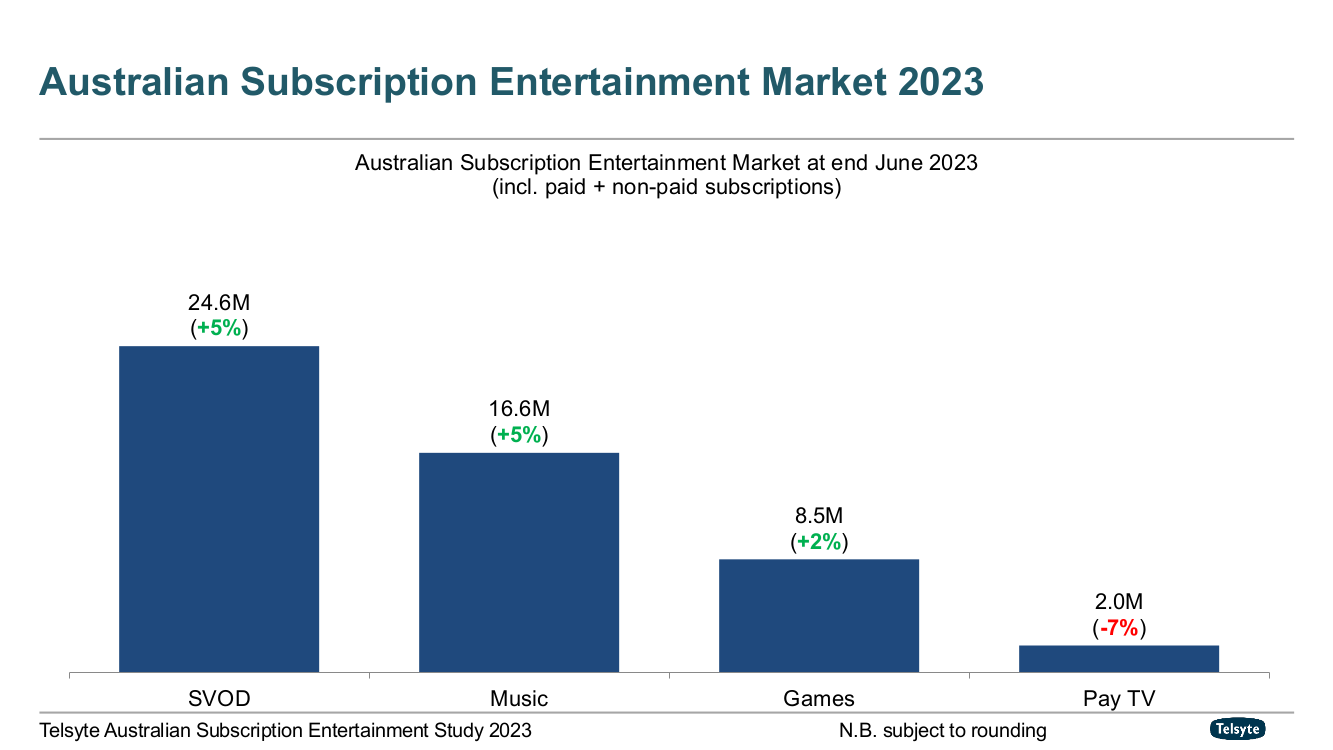

The Telsyte Australian Subscription Entertainment Study 2023 found that the total number of subscription services in Australia increased by 3 per cent to 49.9 million in June 2023. This growth rate is lower than the double-digit increase observed in the previous year. However, the report also revealed that entertainment subscription services remain essential to Australians, with half of them saying that on-demand services are vital to meeting their entertainment needs.

Video competition heats up, Netflix numbers fall

The SVOD segment continued to be the largest and most competitive in the subscription entertainment market, with the number of services reaching 24.6 million in June 2023, up by 5 per cent year-on-year. The average number of SVOD subscriptions per household rose to 3.4, with 39 per cent of subscribing households having three or more services.

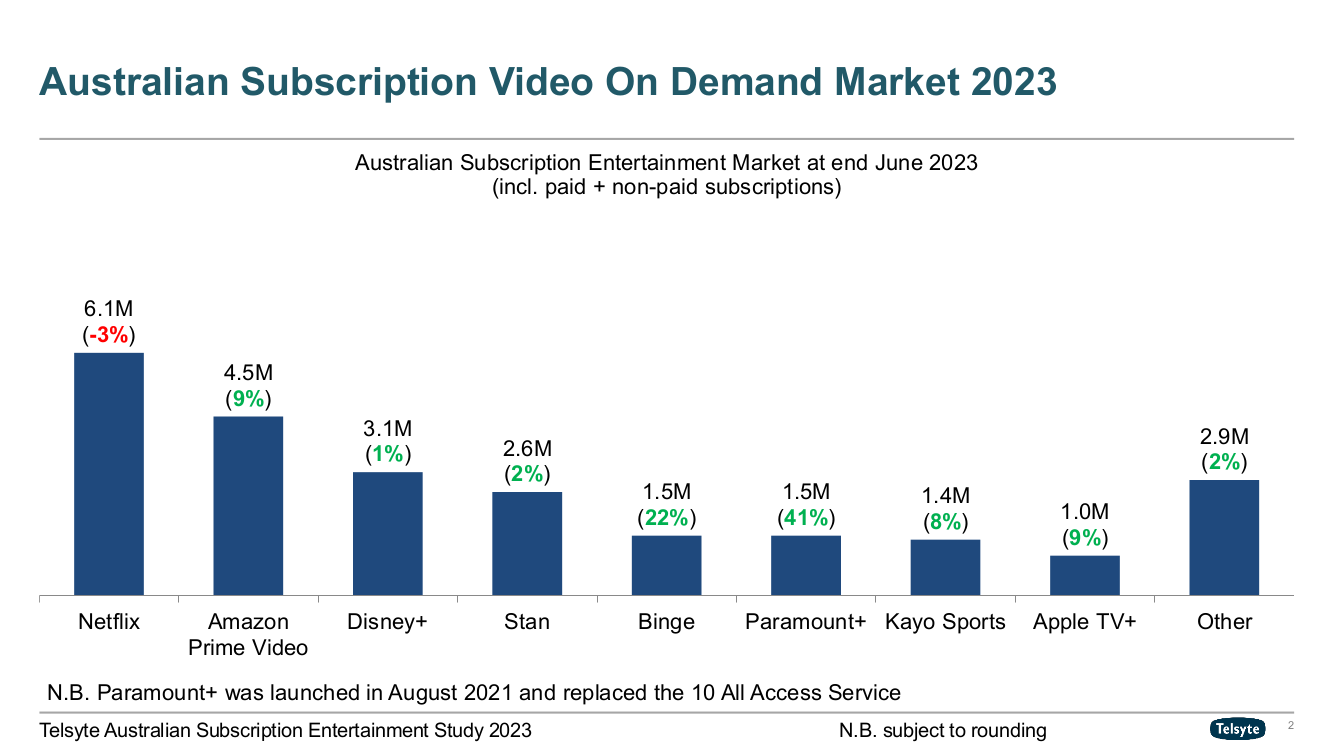

The report found that Netflix, the market leader, experienced its first decline in subscriber numbers in Australia as of June 2023, while others gained ground. The report attributed the decline to the backlash to Netflix's crackdown on account sharing and its introduction of an ad-supported plan, which faced user resistance.

Despite the dip, the study found Netflix (6.1 million) remained the top SVOD service at the end of June 23, followed by Amazon Prime Video (4.5 million), Disney+ (3.1 million), Stan (2.6 million), Binge (1.5 million), Paramount+ (1.5 million), Kayo Sports (1.4 million) and Apple TV+ (1.0 million).

While there has been a slowdown in growth and increased competition, the report showed that SVOD consumption remained strong with over half (55%) of Australians continue to discover new content through their services.

The average total weekly video entertainment consumption reduced by 9 per cent year-on-year to 45 hours from its high in 2022, but consumption of SVOD was one of the only two categories that saw an increase across 9 video categories measured by Telsyte.

However, nearly half (48%) of subscribers claim they are more likely to switch between different services to save money than previously, and only 27 per cent find it difficult to ‘unsubscribe’ their main services even when they don’t use them often.

“Profits, partnerships, and more aggressive behaviour. There’s going to be increasing competition to win people over from other platforms,” Telsyte Managing Director, Foad Fadaghi, says.

Telsyte estimates the total number of SVOD subscriptions could reach over 30 million by June 2027, driven by a new content boom; growth in multiple subscriptions; new market entrants and more ad-supported plans across services.

SVOD market revenue is estimated at $2.7Bn for FY2023, a 14 per cent year-on-year increase driven by subscription cost rises and an increase in service adoption.

The study found that paid SVOD services rank 6th (34%) among areas where consumers would consider reducing spending if their household budget becomes tight (with the top 3 being dining out & takeaway, clothing & accessories, and holiday-related expenses). Notably, only 19 per cent of respondents said they had cut spending on paid SVOD services in the past 12 months, coming in at 10th.

“Paid SVOD services as a category exhibits strong retention and near recession-proof characteristics, as other significant spending areas become household budgeting priorities,” says Fadaghi.

Telsyte found over half (51%) of SVOD users are expecting the price of streaming video services to increase this year and have adjusted their SVOD budget accordingly. Among those willing to pay for streaming video services, the average monthly budget has increased by 7 per cent from a year ago to over $36. The increase is similarly in line with the average CPI inflation recorded in 2023.

Crackdown on account sharing faces user resistance

This year saw the beginning of highly publicised crackdowns on account sharing by streaming service providers, making it harder for people to pay for one account and share access to it between family and friends.

Australians are used to sharing their SVOD services, with the study suggesting that 1 in 3 (32%) SVOD subscribers share their services. Among those sharing services, half (50%) share with others who reside in different households.

The majority (>80%) intend to share services for as long as they can, and the top reason for sharing is to save money (55%). However, 48 per cent of Australians claim they will stop sharing altogether if they are required to pay to share these services.

Around 7 per cent of those who have subscribed to Netflix in the last 12 months ended up cancelling Netflix due to the new rules imposed around sharing with others outside the household. At the time of the survey, the uptake of Netflix’s new extra member plan (as of June 23) had yet to exceed the number of cancellations suggested by the survey findings.

While limiting the shareability outside of account owners’ households might provide additional revenue for service providers, Telsyte sees it as a risk for some providers and a reason consumers might explore competing services.

Free and ad-supported services keep people entertained

Paid-for SVOD is here to stay, but Telsyte’s research also found more than 60 per cent of non-SVOD users believe there is enough good quality video content from free sources to keep them entertained and not have to pay for any subscriptions.

Broadcasting Video on Demand services (BVOD, including 7Plus, 9Now, 10Play, ABC iView and SBS On Demand) remained popular and most platforms had more than 10 million viewers during FY2023.

Additionally, nearly 5 million Australians claim they have used free and ad-supported streaming TV (FAST) services, or services that offer FAST channels in the last 12 months.

Australians now have the option of more affordable ad-supported SVOD plans since Netflix and Binge launched their ad-supported options during FY2023. According to Telsyte’s research, there are more than a million non-sport SVOD subscriptions subsidised by advertisements as of June 2023.

The study found that 36 per cent of SVOD users are interested in more affordable ad-supported service plans. Telsyte believes more services could introduce an ad-supported tier to attract a new audience and ad-supported plans could potentially lift the average number of subscriptions per household closer to 4 (currently 3.4) by 2027.

Support for local content remains strong

The study highlighted significant interest in Australian content on SVOD platforms in the past year with two in three (66%) Australians claiming they have watched locally-developed content on SVOD platforms in the last 12 months, and nearly 60 per cent saying they want to see more.

More than half of SVOD watchers also believe it is important to have content that has Australian stories, voices, culture and values in their services. Additionally, a third (34%) of Australians say they are more likely to subscribe to an SVOD service that continues to support and invest in local film and TV production.

Australians are also voicing their concerns over the recent debate about using generative AI to produce video content, with half (50%) not believing generative AI can replace human screenwriters in creating captivating, distinct storylines that capture their interest. Additionally, 60 per cent say viewers should be made aware of the source of material produced using generative AI in videos, TV shows and films.

More than 3 in 5 (62%) also believe production companies should compensate actors and celebrities (and seek consent) if AI-generated digital replicas are used for content production. Overall, Australians show strong support for the local production industry, with 57 per cent advocating for the regulation of generative AI-produced source material in the video and film sector.

Smaller gaming budgets impacting subscription growth

Australians had taken up 8.5 million games-related subscriptions at the end of June 2023, a 2 per cent increase from a year ago.

Telsyte believes the slowdown is due to consumers having a tighter budget for video games, with a slowdown witnessed across content, services and consoles. The annual average consumer budget for video games has also been reduced by 11 per cent from a year ago.

Microsoft’s Xbox Game Pass remains the leader across all types of games-related subscriptions that Telsyte measures as consumers continue to gravitate towards the all-you-can-play subscription model. The Nintendo Switch Online service saw stronger growth, benefiting from the popular Nintendo Switch consoles among younger Australians.

Interest in cloud gaming remains high with the adoption of cloud gaming outpacing the slowing video game subscription market. Telsyte estimates the number of gamers adopting cloud gaming services such as Microsoft’s xCloud and GeForce Now is approaching a million, an increase of 73 per cent from a year ago. Cloud gaming remains highly sought after amongst hardcore gamers who play video games for more than 3 hours a day.

Music subscriptions maintain modest growth

Streaming music remains popular with the adoption of subscriptions reaching 16.6 million at the end of June 2023, an increase of 5 per cent from a year ago.

The top 3 streaming music service providers in Australia remained Spotify, Google (incl. YouTube Music and YouTube Premium) and Apple Music. More listeners are using Amazon Music as part of the Amazon Prime subscription.

In addition to music, the study found audiobook subscriptions continue to grow steadily, with close to 1.5 million users in June 2023, up from 1.3 million in the prior year.

For further information on the study or media enquiries contact:

Foad Fadaghi

Managing Director

Tel: 1800 313 142

Email: ffadaghi@telsyte.com.au

Alvin Lee

Senior Analyst

Tel: 1800 313 142

Email: alee@telsyte.com.au

The Telsyte Australian Subscription Entertainment Study 2023 is a comprehensive study that provides subscribers with:

Market sizing and forecasts of the Australian entertainment subscriptions market, including video, music, and games

Insights into consumer attitudes and technology adoption trends

Uptake, intention, and detailed analysis of

Video services including: SVOD, pay TV and BVOD services

Streaming music services

Games-related subscription services

Services consumption preference including devices, fixed and mobile service.

Insights into the future of entertainment subscription services in Australia.

In preparing this study, Telsyte used:

An online survey conducted in August 2023 with a representative sample of 1,109 respondents, 16 years and older.

An online survey conducted in December 2022 with a representative sample of 1,036 respondents, 16 years and older.

Interviews conducted with executives from SVOD, Pay TV and video game service providers, content providers, funding agencies and hardware manufacturers.

Financial reports released by service providers and media companies.

On-going monitoring of local and global market trends.

Editor’s note:

Telsyte measures the hours that consumers spend on consuming all types of video content. Examples include FTA TV, SVOD, social media videos, BVOD etc.

Telsyte actively monitors the SVOD services market, including over 40 SVOD services. Other examples include Britbox, CrunchyRoll, Foxtel Now, Hayu, Optus Sport etc.

The measure is the number of subscriptions at the end of June 2023 (snapshot), not usage/utilisation. Content releases will influence the number of subscriptions when measured at different points in time.

Telsyte measures Amazon Prime Video as a subset of Amazon Prime – with measured subscribers self-reporting their use of the video service.

FAST channels are curated scheduled channels that feature specific programs, genres or themes and offer an improved viewing experience of linear TV channels (e.g., a channel that is dedicated to ‘MasterChef’ or ‘shows from the 70s’). Examples of services that offer FAST channels include Samsung TV Plus, Plex, 7Plus, 10Play).

About Telsyte

Telsyte is Australia’s leading emerging technology analyst firm. Telsyte analysts deliver market research, insights and advisory into enterprise and consumer technologies. Telsyte is an independent business unit of DXC Technology. For more information visit www.telsyte.com.au

The material in this article is copyright protected and not intended to be altered, copied, distributed or used for any commercial or non-commercial purpose, except for news reporting, comment, criticism, teaching and scholarship.