Creator economy reaches scale as competition for viewing time intensifies

SYDNEY, AUSTRALIA – Despite housing and cost of living pressures, Australia’s subscription entertainment market grew by 5 per cent to nearly 54.6 million services in the 12 months to June 2025, according to new research from the Australian emerging technology analyst firm, Telsyte.

The Telsyte Australian Subscription Entertainment Study 2025 found Australians are holding onto on-demand entertainment, with 47 per cent of SVOD users calling their service “non-negotiable”, 44 per cent of music streamers saying it is essential, and 63 per cent of committed gamers who play more than three hours a day calling games “must-have”.

The study found even with a maturing market, growth continues across the three main categories of SVOD (5%); streaming music (6%); and games-related subscriptions (7%). Telsyte excluded Optus Sport from its June 2025 reporting given the imminent closure and the ongoing subscriber transition to Stan Sport.

Increasing access options and deals boost SVOD market

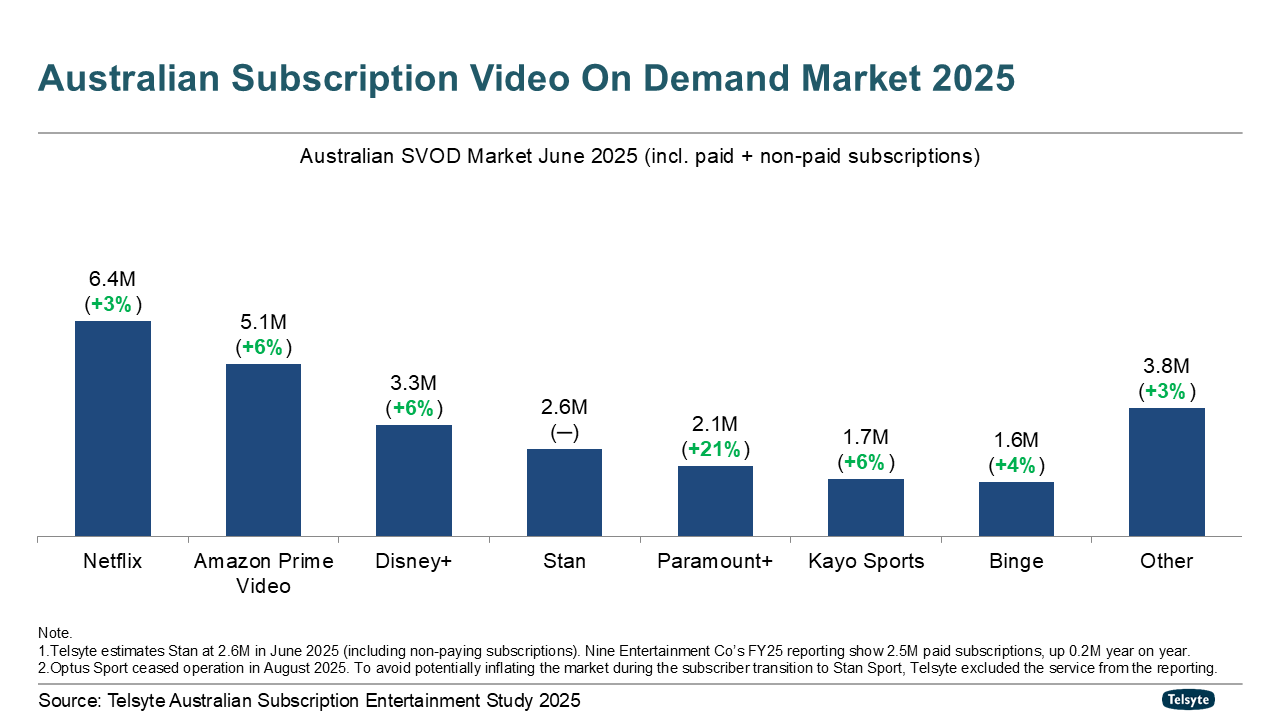

More affordable ad-supported plans, paid sharing (extra member) programs, deals and cross-sector bundles and the launch of HBO Max combined to grow the total number of Subscription Video on Demand (SVOD) services to 26.6 million by June 2025, up 5 per cent year-on-year.

The market leaders remained consistent with Netflix (6.4 million subscriptions) holding the top position, followed by Amazon Prime Video (5.1 million), Disney+ (3.3 million), Stan (2.6 million), Paramount+ (2.1 million), Kayo Sports (1.7 million) and Binge (1.6 million). Paramount+ was the fastest growing major service in FY2025.

Momentum also came from the long tail of other services with fewer than one million subscriptions, fuelled by new entrant HBO Max combined with consumer interest in diversified content and strong appetite for sport.

HBO Max reached the top 10 within just three months of launch, while beIN Sports and Crunchyroll posted the fastest growth spurred on by bundling, and rising anime popularity (Apple TV+ and BritBox also featured in the top 10).

Active subscription management rises as households stretch entertainment budget

The study found Australians are spending more to support multiple subscriptions. Among those willing to pay for streaming video, the average monthly budget jumped 18 per cent (+$6.30) to nearly $42, outpacing the average 13 per cent rise in plan prices from the top 10 services as of September 2025.

About a quarter of subscribers claim they frequently exceed their budget, with subscribing households now carrying 3.3 services on average.

Telsyte Managing Director Foad Fadaghi says SVOD is now an active channel for competitive deals and cross promotions with telecom, utilities, food delivery and financial services.

“Households aren’t walking away from streaming, they are reprioritising and keeping their multi-service setups affordable,” Fadaghi says.

The study found about one in four SVOD subscribers reported encountering such deals in the past year, and most acted on them: on average securing three months of benefits at an average 36 per cent discount.

However, cost-of-living pressures remain evident as value-seeking behaviours intensify, with nearly two-thirds (63%) of Australians report expenses rising faster than income, and 46 per cent SVOD users rotate services more often than last year to manage costs.

Around half the SVOD subscribers say they actively hunt discounts or subscribe for specific titles then cancel afterwards. As a result, the research found exclusive content and frictionless sign-ups are becoming more important than sheer catalogue size when subscribers choose a service.

Ad-supported SVOD subscriptions more than doubled from 2.5 million to 6.4 million, led by Amazon Prime Video’s shift to ads in July 2024, with Netflix, Binge, HBO and Paramount+ also gaining traction as consumers embrace lower-cost access.

Despite the closure of Optus Sport, sport is a growing differentiator for SVOD services. Among Australia’s top SVOD services (excluding dedicated sport services such as Kayo), around one in five subscribers now cite sport as a key sign-up reason.

Consumers also want sport to stay accessible, with 2 in 3 believing access to free sports via free streaming services such as BVOD should be guaranteed for Australians, mirroring existing protections for free-to-air TV.

Local content remains highly valued and the study revealed more SVOD subscribers have seen Australian-related programming than other content. More than half (58%) of subscribers say it is important to have content that represents Australian stories, voices, culture, and values on SVOD services.

Ad-supported and creator-driven video shape the broader entertainment landscape

Telsyte found average weekly video consumption rose by four hours to more than 51 hours, driven by social media, YouTube and free and ad-supported streaming TV (FAST) services.

FAST services are now reaching 2.3 million Australians, growing over 40 per cent from a year ago, led by Samsung TV Plus and followed by LG Channels. FAST’s scheduled, linear-style channels are tapping into Australian’s enduring preference for live viewing, as nearly half of video viewing time is still live (vs. on demand).

Broadcasting Video On Demand (BVOD) services remain popular, exceeding 12 million viewers across 7Plus, 9Now, 10Play, ABC iView and SBS On Demand during FY2025. These apps also feature highly in mobile App Store ranks.

Social media video platforms such as YouTube and TikTok continue to attract mass audiences, with 17 million Australians watching YouTube and 52 per cent doing so daily. Casual and creator-led videos are the big drawcard, feeding into the fast-growing creator economy.

Telsyte estimates the direct-to-creator subscription market is now worth around half a billion ($500 million) annually (excluding adult content and advertising/revenue sharing), as Australians pay to support individual creators on creator-led platforms such as social media, YouTube, Twitch, Patreon and Substack.

Beyond entertainment, three in five subscribers say individual creators deliver insider knowledge and expert insights they cannot get from mainstream sources.

With podcasts an established part of Australians’ digital media libraries, around 9 million people listening to or watching them. The video format is taking off with 6.6 million Australians now watching video podcasts (vodcasts).

This shift reflects the gravitational pull of creator content and more engaging formats. YouTube and Spotify are the current leading podcast platforms. Telsyte expects SVOD and other services to extend into the social media creator world, to reach new audiences.

"There is a shift from platform to affinity discovery, fans now follow creators across formats ," says Telsyte Senior Analyst Alvin Lee.

Streaming music subscriptions growing steadily

Streaming music reached 19 million subscriptions at the end of June 2025, an increase of 6 per cent from previous year supported by population growth and bundled access.

Australia’s top streaming music providers remain Spotify, Google (incl. YouTube Music and YouTube Premium listeners for music) and Apple Music. Amazon Music listenership continues on the rise as more utilising the service as part of the Amazon Prime subscription.

Games-related subscriptions grow as cloud gaming momentum builds

Australians held 9.7 million games-related subscriptions at the end of June 2025, up 7 per cent year-on-year as most services expanded alongside a revitalised console cycle, energised by the Nintendo Switch 2 launch and increasing popularity of handheld consoles.

Microsoft’s Xbox Game Pass remains the leader across Telsyte-tracked games-related subscriptions as consumers embrace the play-anywhere, anytime subscription model.

Interest in cloud gaming remains high, with over one million Australians using services such as Microsoft’s Xbox Cloud Gaming and GeForce Now. Telsyte expects stronger uplift in the coming years as Xbox Cloud Gaming exits beta and expand across more plan tiers and devices, as well as potential local availability of Amazon Luna - Amazon’s cloud gaming platform, included with Prime in some markets.

For further information on the study or media enquiries contact:

Foad Fadaghi

Managing Director

Tel: 1800 313 142

Email: ffadaghi@telsyte.com.au

Alvin Lee

Senior Analyst

Tel: 1800 313 142

Email: alee@telsyte.com.au

The Telsyte Australian Subscription Entertainment Study 2025 is a comprehensive study which provides subscribers with:

Market sizing and forecasts of the Australian entertainment subscriptions market, including video, music and games

Insights into consumer attitudes and technology adoption trends

Uptake, intention and detailed analysis of

Video services including: SVOD, pay TV and BVOD services

Streaming music services

Games-related subscription services

Service and content consumption preferences

Insights into the future of entertainment subscription services in Australia.

In preparing this study, Telsyte used:

An online survey conducted in August 2025 with a representative sample of 1,025 respondents, 16 years and older.

An online survey conducted in July 2025 with a representative sample of 1,001 respondents, 16 years and older.

Interviews conducted with executives from SVOD, Pay TV and video game service providers, content providers, funding agencies and hardware manufacturers.

Financial reports released by service providers and media companies.

On-going monitoring of local and global market trends.

Editor’s note:

Although Optus Sport officially ceased operations in August 2025, Telsyte excluded the service from its June 2025 reporting given the imminent closure and the ongoing subscriber transition to Stan Sport to avoid potentially inflating the market. Excluding the impact of Optus Sport, Telsyte estimates the SVOD market would have grown by around 7 per cent.

Telsyte reports Stan at 2.6 million in June 2025, include non-paying subscriptions. Nine’s reporting shows 2.5 million paid subscriptions, up 0.2 million year-on-year.

Telsyte actively monitors the SVOD services market, including over 40 SVOD services. Other examples include Apple TV+, BritBox, beIN Sports, Crunchyroll, Foxtel Now, Hayu, HBO Max NBA League Pass and etc.

The measure is the number of subscriptions at the end of June 2025 (snapshot), not usage/utilisation. Content releases will influence the number of subscriptions when measured at different points in time.

Telsyte measures Amazon Prime Video as a subset of Amazon Prime – with measured subscribers self-reporting their use of the video service.

Telsyte measures the hours that consumers spend on consuming all types of video content. Examples include FTA TV, SVOD, social media videos, BVOD, FAST services etc.

Examples of FAST services include Samsung TV Plus, LG Channels and Plex. FAST channels are curated scheduled channels that feature specific programs, genres or themes and offer an improved viewing experience of linear TV channels (e.g. a channel that is dedicated to ‘MasterChef’ or ‘shows from the 70s’). FAST channels can also be found on BVOD services such as 7Plus, 10Play, and platforms/services like Fetch and Binge).

The direct-to-creator subscription revenue figure excludes adult content and accounts only for subscription-based revenue, not advertising or platform partner program payouts.

About Telsyte

Telsyte is Australia’s leading emerging technology analyst firm. Telsyte analysts deliver market research, insights and advisory into enterprise and consumer technologies. Telsyte is an independent business unit of DXC Technology. For more information visit www.telsyte.com.au

The material in this article is copyright protected and not intended to be altered, copied, distributed or used for any commercial or non-commercial purpose, except for news reporting, comment, criticism, teaching and scholarship.